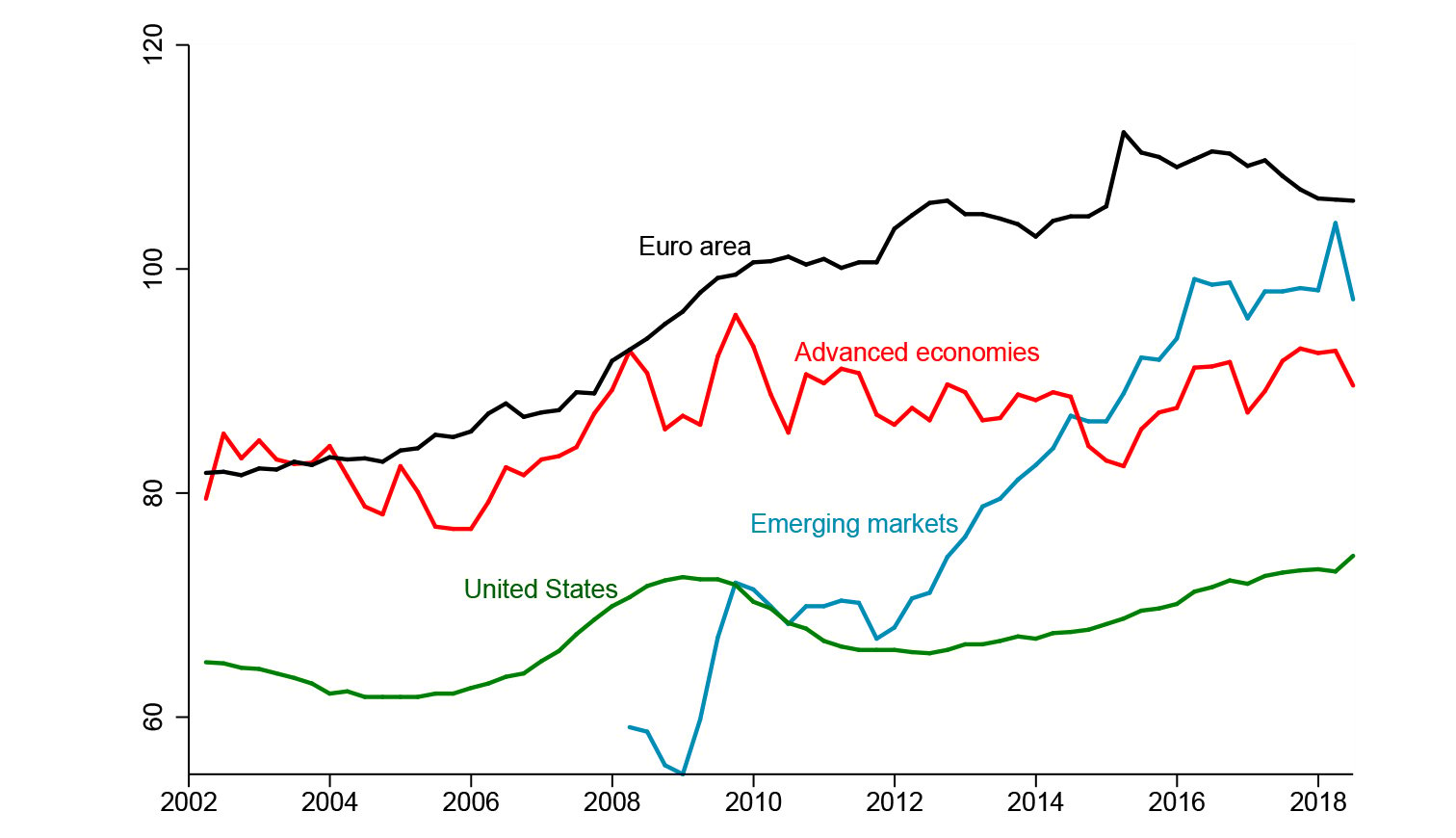

There has been a large increase in corporate leverage in many countries since the early 2000s. Figure 1 plots corporate debt to GDP since 2002 for different groups of countries. With the exception of the U.S., both advanced economies and emerging markets have corporate debt exceeding GDP since 2005. U.S. corporate debt is also on an increasing trend. The fastest growth in corporate debt has been observed in emerging markets. A closer look will reveal that China and other fast growing emerging countries in Asia drive most of the increase in corporate debt for the emerging markets (See IMF (2018)).

Figure 1 Corporate Debt/GDP: Advanced and Emerging Countries

Source: Data from BIS. Figure from Kalemli-Ozcan, Liu, Shim, 2019. |

Should we worry about these trends? I would argue that we should. I will base my argument on three detrimental effects that corporate sector leverage can have on the aggregate economy and society at large. The first effect is that leveraging and deleveraging of corporate sector can lead to boom-bust cycles in the aggregate economy (See Dinlersoz, Kalemli-Özcan, Hyatt, and Penciakova (2018)). The second effect is persistently sluggish aggregate investment if the process of deleveraging goes on too long after a financial crisis (Kalemli-Özcan, Laeven, and Moreno (2018)). And, the third effect is low aggregate productivity. If capital is allocated to the “wrong” firm, then the aggregate productivity can go down overtime. Some firms can borrow easily as they are bigger, have larger net worth, and politically connected, which in turn help them to raise their capital but they are “wrong” firms in the sense that they are not necessarily the most productive firms. These dynamics can lead to misallocation of capital across firms and a declining productivity for the aggregate economy. Gopinath, Kalemli-Özcan, Karabarbounis, and Villegas-Sanchez (2017) document these patterns for the southern European countries during 2000s.

These detrimental effects of corporate leverage will be felt most by the vulnerable groups in the society, young and poor and also middle class. During a deleveraging process, corporates will downsize and will fire first the young and inexperienced workers. In an economy that is characterized with a productivity slowdown and sluggish investment, young entrants and middle-class entrepreneurs will have much harder time to finance themselves and to start new businesses.

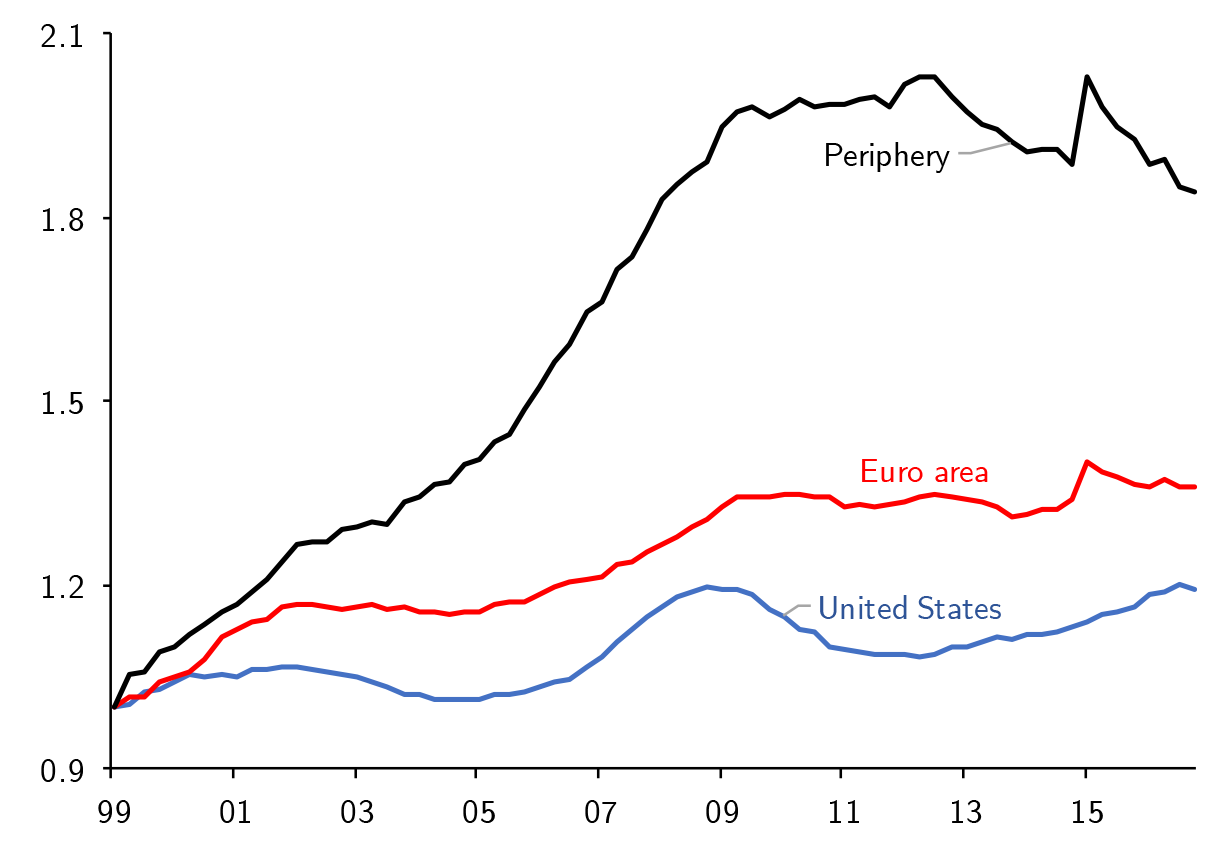

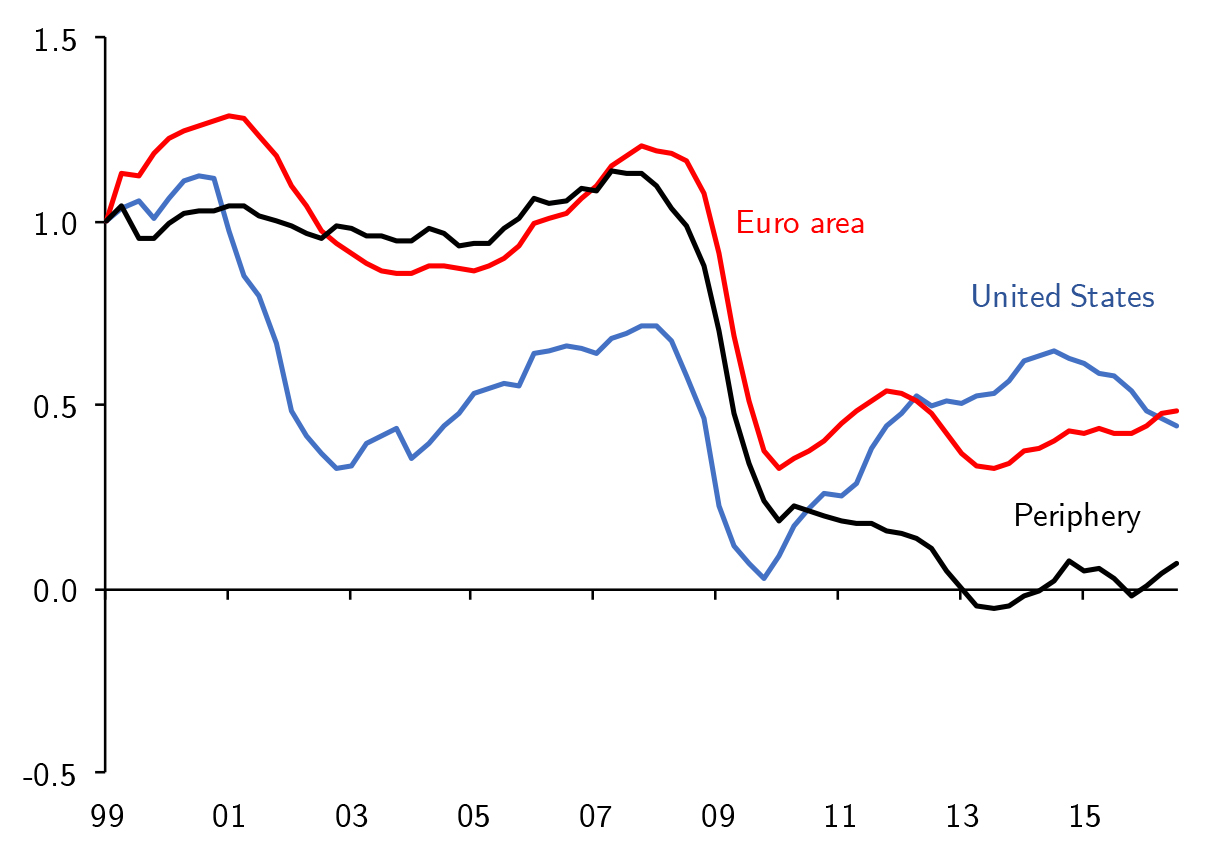

Let me explain each detrimental effect of high corporate leverage in detail. Figure 2a below shows the increase in corporate debt to GDP in the periphery countries of Europe in comparison to the Euro area countries and the U.S. Figure 2b shows the corporate investment to GDP in these countries. Both figures are normalized to 1 in the first year, 1999. It is clear that the periphery countries of Europe (Portugal, Italy, Ireland, Greece, Spain) had the largest increase in corporate debt before the global financial crisis of 2008 and this increase was accompanied by the largest drop in corporate investment after the crisis. If we take a closer look using more granular data at the firm level, we see that firms that entered the crisis with higher leverage in terms of short term debt, decreased investment (and employment) more since they suffered from both a debt overhang problem and a rollover risk problem during and in the aftermath of the crisis. In order to understand the extent of each of these problems, we have to investigate both bank and firm level data. Bernanke (2018) argues that the 2008 financial crisis depressed economic activity in the U.S through firms and banks interaction. The severe downturn is due to the panic in funding and securitization markets, which disrupted the supply of credit to the real economy. This case must be even stronger for the countries of Europe.

Figure 2a Corporate Debt to GDP |

Figure 2b Corporate Investment to GDP |

|

|

Source: Data from BIS, Figure from Kalemli-Ozcan, Laeven, Moreno, 2018.

Matching millions of firms in eight European countries to their banks, Kalemli-Özcan, Laeven, and Moreno (2018) shows that firms who borrowed more during the boom, ended up entering the crisis with higher leverage in terms of short-term debt and this leverage hurt them during the bust. Although such leverage helped firms to finance their investment during the boom years, during the bust, banks cut their lending to these risky firms and refused to roll-over their short-term debt since banks themselves were in trouble. As a result, these firms decreased their economic activity more. Given the advantage of our firm-bank matched data, we also show that the decline in investment for firms who borrowed from weaker banks was even deeper.

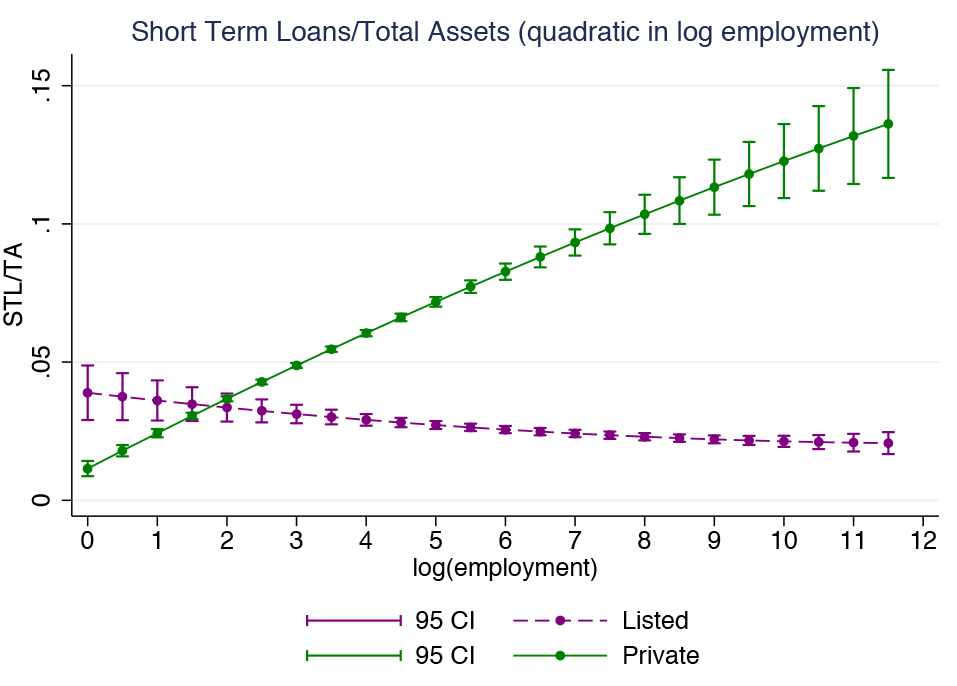

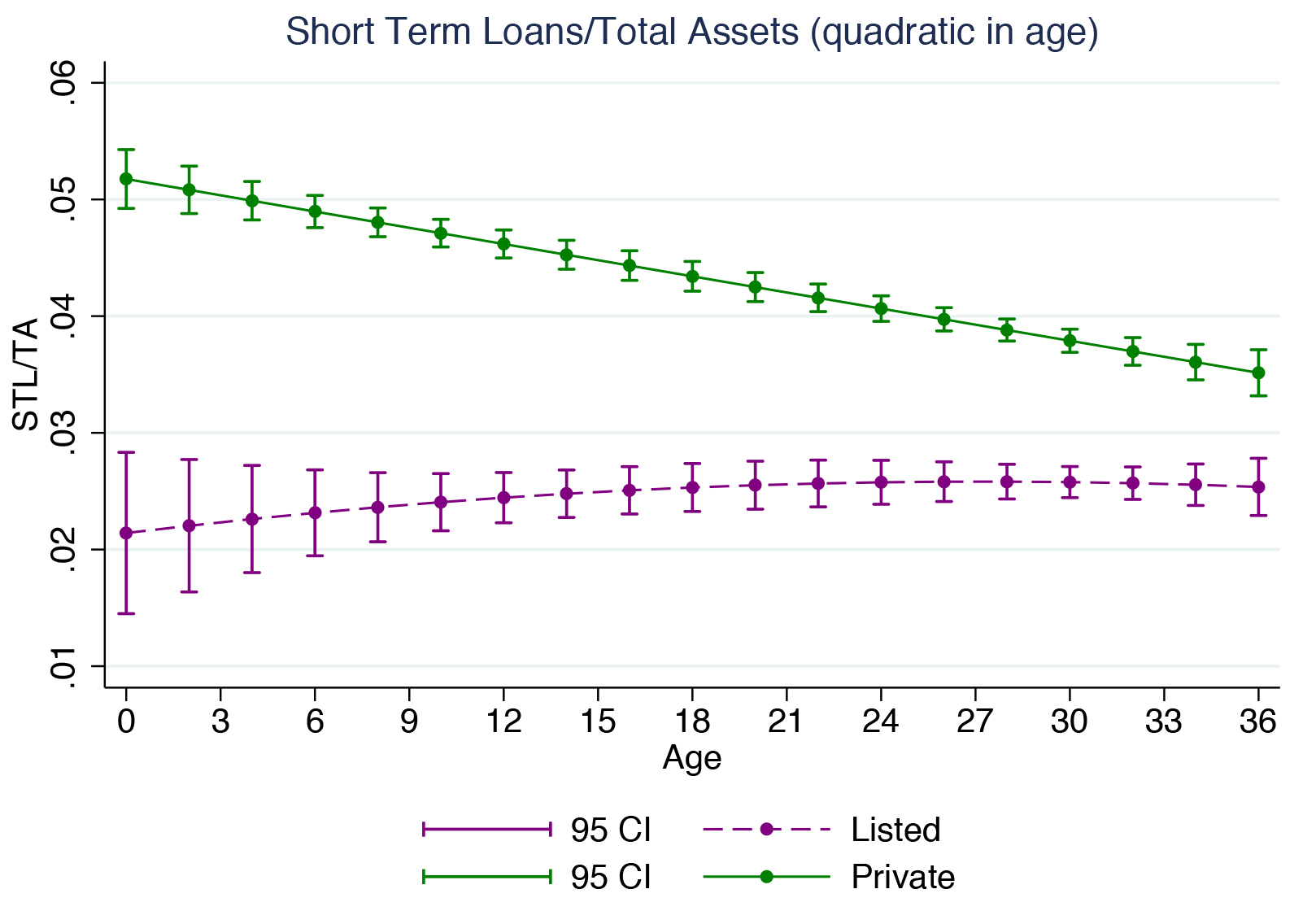

Although the extent of the corporate leverage was not as high as the one in Europe, there is a similar story for the U.S., as argued by Bernanke (2018) and as we show in our research. Corporate leverage in the U.S. has a direct impact on aggregate boom-bust cycles (Dinlersoz, Kalemli-Özcan, Hyatt, and Penciakova (2018)). In the U.S. it is important that we investigate the leverage patterns of both private and public firms since there might be differences as shown in Figure 3a below. While private firms in the U.S. increase their leverage as they get bigger, shown by the green line, there is no significant relationship between firm leverage and size for the publicly listed firms in the U.S. (purple line). In terms of firm age, dynamics also differ as shown in figure 3b. While private firms decrease their leverage as they get older, public firms slightly increase it. These different leverage dynamics of private and public firms have important implications for firm and aggregate growth. Public firms account only for 26 percent of the aggregate U.S. employment and 44 percent of aggregate U.S. output so without understanding the link between private firms leverage and growth, we cannot explain the huge decline in employment and investment that occurred during the Great Recession in the U.S.

Figure 3a Leverage and Firm Size in the US |

Figure 3b Corporate Investment to GDP |

|

|

Source: Data and Figure from Dinlersoz, Hyatt, Kalemli-Ozcan, Penciakova, 2018.

Our research shows that, similar to Europe, in the U.S., private firms who entered the crisis with higher short-term leverage, ended up growing less and cutting down employment more during the crisis. Moreover, sectors with high leverage experienced high employment during the boom but these are also the sectors that experienced larger contractions during the bust and ended up with more lay-offs.

It is clear that during the boom, firms both in Europe and in the U.S. financed themselves with short-term debt, increasing investment and employment. However, this short-term debt based leverage hunted them during the bust, causing them to decrease investment and employment more so that they can de-lever, bringing down the aggregate economy with them. To be able to prescribe the right policies to remedy this problem, we have to understand first why firms finance themselves with short-term debt during the boom. There might be several reasons but an important one is the low interest rates that make borrowing cheap.

The boom period in Europe coincides with the introduction of the Euro in 1999 and a fast integration process that drove down the firms borrowing rates, especially in the periphery countries from over 8 percent to a mere 2 percent in few years. In the U.S., after the recession of early 2000s, the interest rates were reduced and kept low for an extended period of time. In such an environment, the rational reaction is to borrow and increase investment since the return to saving (interest rates) and the cost of borrowing that finances investment (interest rates) are both low. To many, such an environment may sound good as access to finance will be improved. However, if the declines in the interest rates are happening in an environment with financial frictions, then not everyone can increase borrowing and investment since smaller firms who lack sufficient collateral may not be able to borrow even they want to borrow. These dynamics will lead to the third detrimental effect that I have mentioned above, that is misallocation of capital and associated productivity decline in the aggregate economy. Pioneered by Restuccia and Rogerson (2008) and Hsieh and Klenow (2009), the misallocation literature documents large differences in the efficiency of factor allocation across countries and the potential for these differences to explain observed productivity differences. Our research contributes to this literature by showing the effect of financial frictions on such misallocation when firms faced with low borrowing costs. As long as not all the firms who can borrow are the most productive ones, then the economy-wide capital will be misallocated. Our data shows that firms who are not the most productive but the largest were able to borrow more and increase their leverage since they have more collateral.

There is a large literature that have endogenized productivity as a function of financial frictions in dynamic models. A typical prediction of these models is that a financial liberalization episode is associated with capital inflows, a better allocation of resources across firms, and an increase in productivity growth (see, for instance, Buera, Kaboski, and Shin, 2011; Midrigan and Xu, 2014; Buera and Moll, 2015). However, a positive shock to access to finance because of financial liberalization, does not match the experience of countries in South Europe where productivity growth declined. We show that contrary to a financial liberalization shock, the decline in the real interest rate is associated with an inflow of capital can lead to a decline in productivity in the short run if a group of productive firms were subject to financial frictions. As long as the borrowing constraint depends on firm size, that is larger firms can borrow more, and where some of these firms are not so productive, then it is straightforward to get the patterns we observe in the data out of a simple model.

The first order policy implication is to better the financial system so that the most productive firms get the funds, not the largest. One way to achieve this is through bank regulation. In another EfIP piece by Admati (https://econfip.org/policy-brief/towards-a-better-financial-system/), these issues are covered extensively so I will not get into the details of bank regulation here. I will highlight the importance of having an inclusive financial system, however, where access to fund should first depend on potential of the project and the existing productivity of the firm, more than anything else. One might think that, this is exactly what state-contingent equity contracts will achieve. However such contracts are not widespread. As argued in another EfIP piece by Mian (https://econfip.org/policy-brief/how-to-think-about-finance/), there are several reasons for this, one being shareholders preferring leverage (as shown by Admati et al. 2018). Another reason is the U.S. tax code that offers deductions which reduces the cost of debt.

Policy makers can clearly change the tax code and regulate the banks to make sure there is not excessive leverage in the system, not only by financial institutions but also by non-financial firms since the latter group will have a direct impact on the employment outcomes. However, in general, the time to change the policies are almost always after bad things happen, such as BASEL regulation after the Great Recession, or the financial stability regulation in Europe after the crisis. One of the key points of my research is that being careful during the good times, especially during low interest rate environments. We need to monitor, what type of loans banks extend to what type of firms during booms, when firms finance investment with short-term debt. This is especially the case for small firms who do not have access to equity financing. Hence, financial regulation should not only worry about capitalization in the banking system, and the volume of equity the system has, but also the quality of the loans made and to whom they were made. Especially, in a rising leverage environment for the corporate sector, these issues must be at the top of the to-do list of the regulators who regulate the intermediaries who make these loans.

How about emerging markets? The figure 1 above shows that the fastest increase in corporate leverage happened in the emerging markets. It is also going to be the case that lower interest rates facilitated by capital flows from advanced countries to emerging markets will make borrowing cheaper. However, there is an additional dimension tied to exchange rate fluctuations.

There are two channels that will link capital flows to corporate leverage in emerging markets. First one is the funding cost/borrowing cost channel, where as a result of capital flows, banking sector in emerging markets can extend lower borrowing rates to firms as they fund themselves cheaply in the international markets (See di Giovanni, Kalemli-Özcan, Ulu and Baskaya (2018)). Second one is the exchange rate channel, where again as a result of capital flows, emerging market currencies appreciate vis-à-vis the dollar and hence emerging market firms who borrow in dollars but have their assets in local currency experience a positive net worth shock via the currency mismatch on their balance sheets (See Bruno and Shin (2015a and 2015b)).

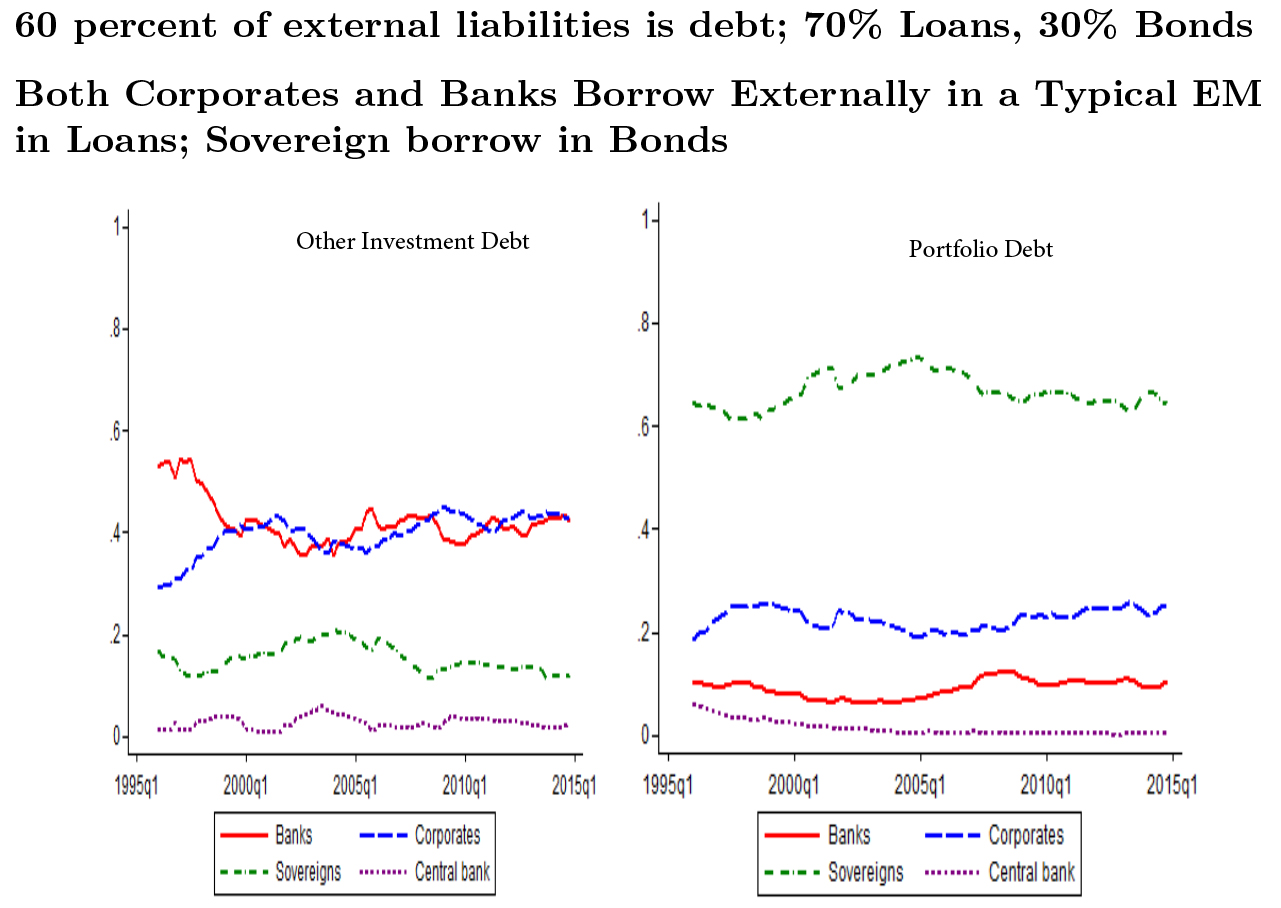

Figure 4 Which Sector Capital Flow Into? (Emerging Markets)

Source: Data from BIS, IMF. Figure from Avdjiev, Hardy, Kalemli-Ozcan, Serven, 2018. |

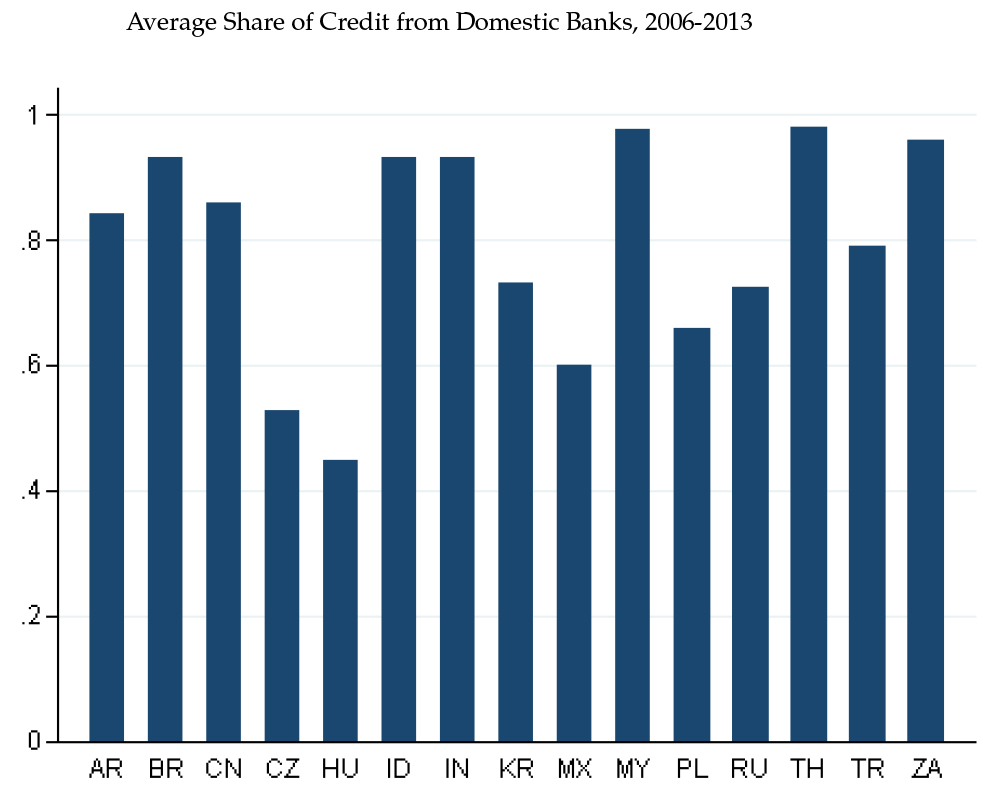

Most of the external borrowing of a typical emerging market is in form of debt and most of this debt is in other investment flows (See Avdjiev, Hardy, Kalemli-Ozcan, Serven, 2018). If we decompose the other investment flows into borrowing by banks, corporates and sovereign sectors as shown in Figure 4, we see that most of that external borrowing will be banks and corporates, shown with red and blue lines for the decomposition of other investment debt. When we look at the portfolio debt flows in the second panel of Figure 4, we see that this is mainly an asset class that emerging markets sovereigns borrow. Hence most emerging market corporates do not issue external bonds but they mainly borrow from external and domestic banks in loans. Figure 5 shows this clearly where most of the corporates in emerging markets borrow from their domestic banking sector. Hence, in combination Figures 4 and 5 imply that domestic banking sectors have a big role in intermediating capital flows to domestic firms in emerging markets. This means the role of lower interest rates will be important for higher leverage also in emerging markets.

Figure 5 Domestic Bank Credit/Corporate Debt

Source: Data from BIS. |

At the same time, capital flows lead to an appreciation of the local currency. Figure 6 shows the share of corporate debt in emerging markets that is in foreign currency (FX). An appreciation of the local currency can increase the borrowing capacity of the corporates in emerging markets who have some of their debt in foreign currency. In fact, we find in our research that, with appreciations over 10 percent, corporates who operate in countries with a higher share of the debt being in foreign currency increase their leverage more. The policy should limit dollar borrowing in emerging markets, especially by regulating domestic banks lending in foreign currency given the key role of capital flow intermediation played by the domestic banks.

Figure 6 Foreign Currency Debt/Non-Financial Sector Debt

Source: Data from BIS. Figure from Kalemli-Ozcan, Liu, Shim, 2019. |

Let me be very clear that, the above findings do not imply a control over the exchange rate or endorse fixed exchange rate regimes. On the contrary, as shown in Kalemli-Ozcan (2019), countries who try to manage their exchange rates in the face of capital flows related spillovers, end up with lower growth so managing the exchange rate is a counterproductive policy. Limiting the exchange rate volatility exactly during sudden stops can have negative and long lasting implications that will hurt long-run growth rate of the country.

What other policy options are available to countries then? Countries can act on the transmission channel cyclically by limiting credit growth and leverage during the booms and doing the reverse during downturns. This can be achieved by the use of macroprudential policies and bank regulation as argued above. So far, the literature has not shown a strong impact from macroprudential policies though the jury is still out as most of these policies were put in place after the crisis and we have yet to see the next big crisis. Again, I would like to be clear that, with macroprudential policies, I mean policies that deal explicitly with excessive leverage in the financial and non-financial sectors in a given economy and not capital account management measures or capital controls. As shown in Kalemli-Ozcan (2019), capital account management policies, in general, go through a form of exchange rate management and these policies end up increasing the extent of dollar debt in the economy, being counterproductive. Instead of preventing capital flows coming in, the policies that limit un-hedged foreign currency denominated liabilities not only in the financial sector but also in the non-financial corporate sector must be a priority. For example, countries like Turkey and Korea regulate the financial sector in terms of un-hedged foreign currency liabilities, where banks cannot have open FX positions without a derivative in place but this is not the case for non-financial firms. Countries like Brazil regulate both financial and non-financial firms and only allow exporters to borrow and keep un-hedged foreign currency liabilities. At the other extreme, countries like Peru does not regulate any sector, but employ exchange rate management policies, and ended up with the largest increase in foreign currency denominated liabilities in the last decade. The rationale for capital account and exchange rate management policies is to provide insulation from spillovers that arise from balance sheet effects of exchange rate fluctuations with large levels of un-hedged foreign currency denominated debt. Kalemli-Ozcan (2019) shows that it is better to deal with this debt directly rather than to try to use a relatively blunt instrument like monetary policy to affect the exchange rate.

However, dealing with excessive credit growth and foreign currency denominated debt may not be enough. A long-term objective that would act on the transmission channel structurally entails reducing the inherent country risk. As shown Alfaro, Kalemli-Ozcan, Volosovych (2008) countries’ institutional quality is the most important causal factor for capital flows in the long-term. High quality institutions will also reduce the risk-sensitivity of capital flows in the short-run. Improvements in the quality and transparency of institutions will reduce idiosyncratic country risk and reduce the sensitivity of capital flows to foreign investors’ risk perceptions. Policies aimed at strengthening the protection of property rights, reducing corruption, and increasing government stability, bureaucratic quality, and law and order should be a priority for policymakers seeking not only to increase capital inflows but also to reduce the sensitivity of capital flows to risk. These policies will also help countries to get the most out of capital flows in terms of sustainable growth, tilting capital flows towards longer maturity debt, and foreign direct investments. Strong institutions will also provide the needed credibility for implementing desirable macroprudential policies, to dampen the severe effects of leverage cycles.

References

Admati, DeMarzo, Hellwig, “The Leverage Ratchet Effect,” The Journal of Finance, 2018, 73 (1), 145-198.

Albuquerque, Rui and Hugo A. Hopenhayn, “Optimal Lending Contracts and Firm Dynamics,” The Review of Economic Studies, April 2004, 71 (2), pp. 285–315.

Alfaro, L., S. Kalemli-Ozcan, and V. Volosovych, “Why Doesn’t Capital Flow from Rich to Poor Countries? An Empirical Investigation,” The Review of Economics and Statistics 2008, 90 (2), 347–368.

Bernanke, Ben, “The Real Effects of the Financial Crisis,” Brookings Papers on Economic Activity, September 2018.

Bruno, Valentina and Hyun S. Shin, “Cross-Border Banking and Global Liquidity,” Review of Economic Studies, 2015a, 82 (2), pp. 535–564.

Bruno, Valentina and Hyun S. Shin, “Capital Flows and the Risk-Taking Channel of Monetary Policy,” Journal of Monetary Economics, 2015b, 71, pp. 119–132.

Buera, Francisco J., Joseph P. Kaboski, and Yongseok Shin, “Finance and Development: A Tale of Two Sectors,” American Economic Review, August 2011, 101 (5), pp. 1964-2002.

Buera, Francisco and Benjamin Moll, “Aggregate Implications of a Credit Crunch: The Importance of Heterogeneity,” American Economic Journal: Macroeconomics, July 2015, 7 (3), pp. 1-42.

Cooley, Thomas, F., and Vincenzo Quadrini, “Financial Markets and Firm Dynamics,” American Economic Review, December 2001, 91 (5), pp. 1286-1310.

Davis, Steven J., John Haltiwanger, and Scott Schuh, “Small Business and Job Creation: Dissecting the Myth and Reassessing the Facts,” Small Business Economics, August 1996, 8 (4), pp. 297–315.

Di Giovanni, Julian, Şebnem Kalemli-Özcan, Mehmet Fatih Ulu, and Yusuf Soner Baskaya, “International Spillovers and Local Credit Cycles,” NBER Working Paper, September 2018, No. 23149.

Dinlersoz, Emin, Şebnem Kalemli-Özcan, Henry Hyatt, and Veronika Penciakova, “Leverage over the Life-Cycle of U.S. Firms,” NBER Working Paper, October 2018, No. 25226.

Gopinath, Gita, Şebnem Kalemli-Özcan, Loukas Karabarbounis, and Carolina Villegas-Sanchez, “Capital Allocation and Productivity in South Europe,” The Quarterly Journal of Economics, November 2017, 132 (4), pp. 1915-1967.

Hugo A. Hopenhayn, “Entry, Exit, and Firm Dynamics in Long Run Equilibrium,” Econometrica, 60 (5), September 1992, pp. 1127-1150.

Hsieh, Chang-Tai and Peter J. Klenow, “Misallocation and Manufacturing TFP in China and India,” The Quarterly Journal of Economics, November 2009, 124 (4), pp. 1403-1448.

International Monetary Fund, “Global Financial Report: A Bumpy Road Ahead,” Washington, DC, April 2018.

Jovanovic, Boyan, “Selection and the Evolution of Industry,” Econometrica, May 1982, 50 (3), pp. 649-670.

Kalemli-Ozxcan, Sebnem, “U.S. Monetary Policy and International Risk Spillovers,” Jackson-Hole symposium 2019, forthcoming.

Kalemli-Özcan, Şebnem, Luc Laeven and David Moreno, “Debt Overhang, Rollover Risk, and Corporate Investment: Evidence from the European Crisis,” NBER Working Paper, November 2018, No. 24555.

Kalemli-Özcan, Şebnem, Xiaoxi Liu and Ilhyock Shim, “Exchange Rate Appreciations and Corporate Risk Taking,” BIS Working Papers, March 2018, No. 710.

Midrigan, Virgiliu, and Daniel Yi Xu, “Finance and Misallocation: Evidence from Plant-Level Data,” American Economic Review, February 2014, 104 (2), pp. 422-58.

Moll, Benjamin, “Productivity Losses from Financial Frictions: Can Self-Financing Undo Capital Misallocation?” American Economic Review, October 2014, 104 (10), pp. 3186-3221.

Restuccia, Diego and Richard Rogerson, “Policy Distortions and Aggregate Productivity with Heterogeneous Establishments,” Review of Economic Dynamics, October 2008, 11 (4), pp. 707-720.

Share: