Note: please read the addendum for the costs of the policy proposed.

The Covid-19 outbreak is a health shock rather than a standard slowdown in economic activity. It is materializing as an unavoidable temporary economic paralysis, and its consequences will likely amount to a severe contraction of the global economy and a global financial crisis. The collective attempts to avoid the spread of the virus are needed desperately, but such containment action will also likely lead to an almost full suspension of economic activity in many parts of the economy.

The recourse to standard expansionary fiscal and monetary policies may not be effective right now. Textbook expansionary policies try to stimulate demand, but people who simply stay at home are not currently responsive to such stimulus, which may in fact reduce these policies’ fire-power when it is needed later on. A “war time” economic thinking should dictate that the virus is the external enemy and needs to be defeated at all costs to recover an economy that functions in a regular way. It calls for a host of targeted policies, as suggested by the IMF Chief Economist Gita Gopinath early on.[1]

Part of this thinking is about figuring out the essence of the shock and its economic transmission in the short run. For macroeconomists, the crisis appears to currently materialize both as a demand shock and a supply disruption. It is also important to pin down whether the shock will lead to a liquidity or a solvency problem for the real sector.

A pure liquidity problem arises when one learns that the return coming today will instead come tomorrow; all that is needed is to manage liquidity accordingly, for example through a loan. A pure solvency problem is associated with a lack of long-term viability. Solvency issues do likely not apply to the majority of the businesses affected by the current paralysis. Once the epidemic is over and the economy recovers, most businesses should be as profitable as before. SMEs, however, may now go bankrupt. The effects from such default are well known: lay-offs, NPLs, weaker banks, weaker demand, sluggish investment, and a sluggish recovery.

Thus, the losses of the economic paralysis should be shared. Preserving the medium and long term continuity of businesses is important for the society.

How to address the liquidity squeeze faced by small businesses?

Several governments have already taken decisive action to address companies’ looming liquidity shortfalls. As a notable example, the German government was quick to legislate a package of economic measures, which includes tax deferrals, as well as unlimited access to loans via Germany’s state owned development bank KfW.[2]

While these policies are extremely welcome and legislation was rapid, there might still be an issue on the magnitude and timely implementation. First, tax deferrals will allow business to delay payment of outstanding tax liabilities. There is large variation across firms in how the magnitude of these liabilities compares to the dramatic reduction in revenues from the contraction in economic activity.

Second, it is unclear whether the administrative process involved in asking for emergency loans can be executed timely enough. For example, will the owner of a small café or a laundry store be able get access to such an emergency loan to service outstanding payments while demand has already virtually collapsed to zero?

Alternative: An immediate negative lump sum tax for SMEs

Many firms need liquidity urgently, it is a matter of weeks or even days. What if the government provides small businesses with an immediate negative lump sum tax?

The magnitude of this government transfer could be determined as a share of the firms’ revenues in 2019 (or a share of an average over past years). How high the share should be (it could in principle be 100% or even above) would depend on how much the government is willing to spend on the program.

The negative tax could come with some conditionality, for example could require firms to hold on to their employees. Thus an alternative way of implementing it, instead of transferring the revenue, can be to transfer the entire payroll wages based on the 2019 tax filings of the firms. For the next year if the company shows lower employment, then the difference can be returned to government. It could be targeted to a subset of firms or industries, ideally to firms below a certain employment threshold such as 500 who constitute small businesses, as for these firms the implementability constraint of the existing measures, pointed out above, likely binds. As argued, it could either come as full-on transfer (pretty much making it “helicopter money”) or it could be partly reversed in later tax years, when the economy has recovered.

A negative lump sum tax can be implemented fast and translates into cash flow for businesses

A negative lump sum tax would allow a cash transfer of a magnitude that could exceed that of a deferral of existing tax liabilities. Importantly, immediate means that the government literally directly wires the money to the business’ bank account via the existing tax system infrastructure, right now! It could be done without requiring firms to do any paper work whatsoever.

In the case of the US, this may be implemented directly via the Internal Revue Service (IRS). Upon successful legislation, the IRS, which should have the required information and infrastructure, could transfer money within days, the way it would do with a standard tax refund.

The government as “buyer of last resort”

The proposal closest to ours has been advocated by Emmanuel Saez and Gabriel Zucman.[3] We very much share their reasoning that an aggressive intervention is needed to prevent mass liquidation of businesses and mass layoffs of workers. Saez and Zucman also acknowledge that access to loans is not sufficient to provide a direct compensation of losses.

Our proposal of a negative tax has the benefit that practical implementation may be swift. For small businesses the problem is a lack of cash and time is already running out. Even if there is the political will to help these businesses, it is logistically tricky to actually send money to firms. Among the different institutions, it should be tax authority has the information and infrastructure needed for this. When the threat of bankruptcy is so immediate, it comes down to practical details such as having a database with the firms’ identities and bank account numbers which can be further linked to the U.S. Census database of the universe of firms.

We are aware that this is a rather blunt proposal, however we believe that out-of-the box thinking is urgently needed now. We also acknowledge that there are some parameters to be figured out, such as the type, magnitude and the universe of firms to be targeted. But the basic idea has the crucial benefit that it would directly and immediately address the disruptive liquidity needs of small businesses, where most employment occurs, and where we therefore think policy intervention currently has the most kick.

Policy is hopefully moving in the right direction

At today’s press conference, Treasury secretary Mnuchin mentioned that in addition to delaying payroll taxes, the US government now aims to provide cash to businesses and individuals, without getting into details. Our proposed policy of a negative lump sum tax, implemented through the IRS, can achieve exactly this in a quick manner. As we write, additional advice by macroeconomists, given with impressive dedication and at an unprecedented speed through social media, points in a similar direction, for instance by calling for a direct “liquidity life line” to European firms via loans from the EIB.[4] It is clear that economists hope to see an aggressive response by policy makers, which takes their advice seriously.

Endnotes

[1] https://voxeu.org/content/limiting-economic-fallout-coronavirus-large-targeted-policies

[2] See details here: https://www.bundesfinanzministerium.de/Content/DE/Pressemitteilungen/Finanzpolitik/2020/03/2020-03-13-download-en.pdf?__blob=publicationFile&v=2

[3] See details here: http://gabriel-zucman.eu/files/coronavirus.pdf

[4] See this very recent piece circulated by Markus Brunnermeier, Jean-Pierre Landau, Marco Pagano and Ricardo Reis: https://scholar.princeton.edu/sites/default/files/markus/files/covid_liquiditylifeline.pdf

Addendum

Supporting US SMEs during the pandemic: how much money gets us how far?

Both policy makers and the public are only beginning to grasp the full scope of the Covid-19 outbreak. While the economic activity needs to be reduced to avoid the spread of the virus, policy makers are intervening through various channels to give support to the economy. Strong interventions are justified based on the idea that the pandemic is temporary and liquidity rather than long-term viability issues are threatening households and firms.

Several economists have called into question textbook Keynesian stimulus measures as providing sufficient support to the economy during this unprecedented disruption.[1] Standard expansionary fiscal and monetary measures, so the reasoning goes, are not enough when people simply stay at home and economic activity is completely suspended. Those measures could be more effective later on, as the economy recovers from the pandemic as standard macroeconomic policy instruments may be conducive to a less sluggish recovery.

In a recent policy brief, Drechsel and Kalemli-Ozcan (March 17, 2020), we suggest a specific measure to support small and medium enterprises (SMEs).[2] We call for decisive action to fight firms’ looming liquidity shortfalls and go as far as proposing a negative lump sum tax. We floated this idea because we worry that some existing policies targeted towards SMEs — tax deferrals and emergency loans — may fall short in terms of size and rapid availability. A negative lump sum tax would allow an actual cash transfer, and immediate means that the government literally directly wires the money to the business’ bank account. This can be done, we argue, via the existing tax system infrastructure, the IRS in the case of the US.

How much money is needed?

In the following analysis, we want to substantiate our proposal by providing some quantitative analysis for the United States. The idea is to answer the question of how much money would get us how far in supporting US SMEs? To investigate this question, we resort to publicly available data from the US Census Bureau.

We previously suggested that the negative tax could be calculated either based firms’ revenues or based on their payroll. Since payroll is typically the largest cost item for businesses, and job losses started piling up, we now focus on the payroll. Note that the UK, for example, has now decided to cover 80% of wages for employees that cannot work because of the outbreak of the virus.[3]

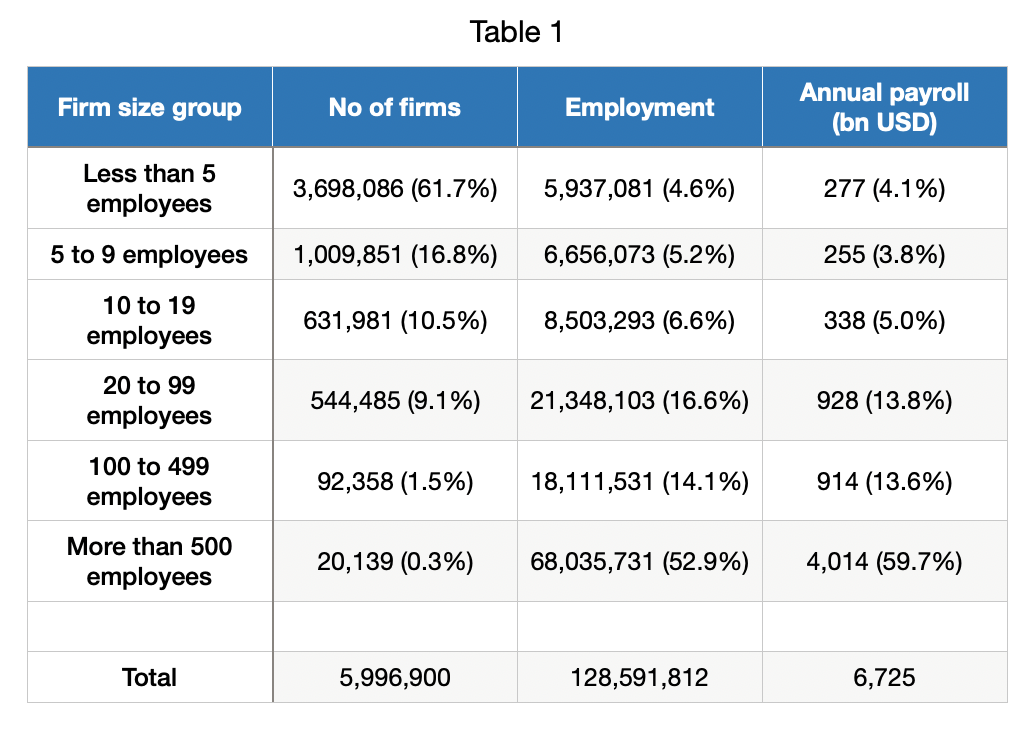

We think that the numbers we provide below are useful even beyond our specific proposal. They could be helpful in putting other policies targeted at US businesses into a quantitative context. Table 1 presents statistics on employment and the size of the payroll across the US firm size distribution for the year 2017.

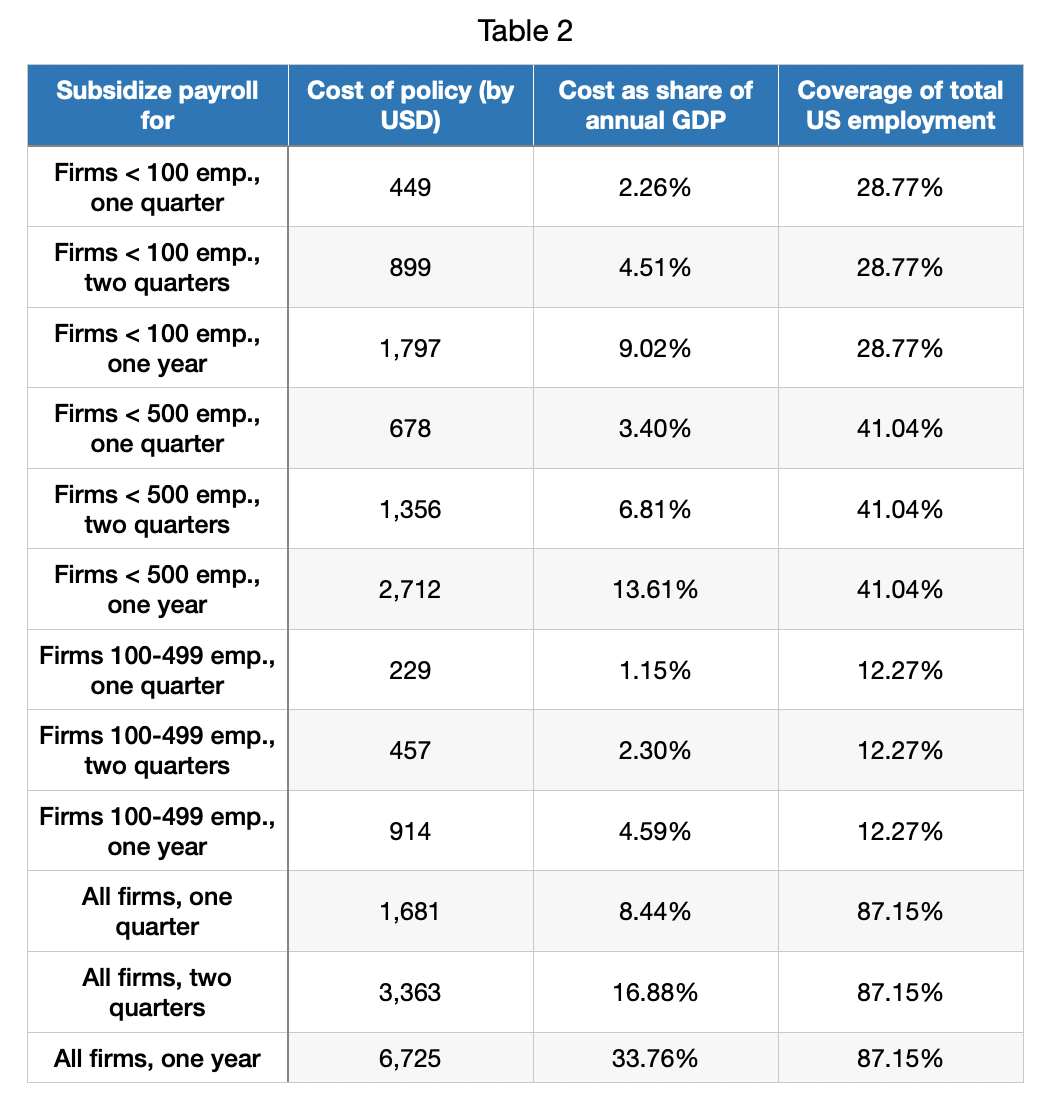

It is visible in Table 1 that a large bulk of US employment is accounted for by relatively small firms. Based on the information in Table 1, we provide calculations for different “policy scenarios”. In each scenario, we postulate that a certain group of firms (as defined by their size in terms of number of employees) receives direct cash payments to cover their payroll for a specific time period: one quarter, two quarters or a year. How costly would these policies be? Table 2 gives the answer by providing the corresponding calculations. To put dollar values into context, we show the cost of potential support policies as a share of US GDP and also include the employment numbers that would fall under a given policy as a share of total US employment.

Can the United States afford an intervention?

We believe that Table 2 provides a useful guideline to contextualize the magnitude of potential support payments to US SMEs. Suppose congress is willing to cover the entire payroll of all firms with more than less than 500 employees for 3 months. This policy would cover the wage bill of 61 Million US workers! This would cost around 3% of US annual GDP. Relative to the losses that are looming from businesses shutting down and workers loosing their job, we do not think the numbers in Table 2 are large enough for policy makers to shy away from aggressive policy. The policy can be made conditional on firms keeping the workers on their payroll and if not then the difference can be returned to the government during next year’s filing.

We also want to stress in that the calculations above, we abstract from general equilibrium effects. In particular, any intervention of the sort we suggest will likely have some multiplier effect. A given firm’s costs are in principle likely to include another firm’s revenue. If a given firm can cover their cost instead of delaying payment or defaulting, this will likely help other firms. Furthermore, making sure that firms will be able to cover their wage bill will put money in households’ pockets and alleviate additional negative effects of the contraction through the labor market.

Endnotes

[1] Some of the proposals made by academic economists are listed here: https://econfip.org/#

[2] The proposal is available at: https://econfip.org/policy-brief/are-standard-macro-policies-enough-to-deal-with-the-economic-fallout-from-a-global-pandemic/

[3] See details here: https://www.theguardian.com/uk-news/2020/mar/20/government-pay-wages-jobs-coronavirus-rishi-sunak?CMP=share_btn_tw

Share: